FAST-DS 2026 provides a one-time compliance window to enable taxpayers to disclose foreign assets or pay the tax on any income arising on Employee Stock Options Plans (ESOPs) and Restricted Stock Units (RSUs). This may arise from foreign employment, low-value or dormant foreign bank accounts of former students, savings or insurance policies for returning non-residents Indian to India and assets held by individuals on overseas deputation.

Applications of Small Taxpayers Scheme (FAST-DS 2026)

Related Read: Why Must Women Make a Will?

FAST-DS 2026 is a special time-frame scheme for resident small taxpayers to disclose foreign assets disclosure and foreign-sourced income. The tax is based on the nature and source of acquisition and grant of immunity from penalty and prosecution under the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 (Black Money Act). FAST-DS 2026 shall remain open for taxpayers for six months from the date of its notification by the Central Government in the Official Gazette.

Categories of Taxpayers to be Benefited by FAST-DS 2026

- Resident taxpayers who failed to furnish their return of income under section 139 of the Income-tax Act, 1961 (Act).

- Resident taxpayers who failed to disclose foreign asset disclosure or foreign income in return of income filed under section 139 of Act before commencement of this scheme.

- Resident taxpayers have foreign assets or foreign income which have income escaping assessment within the meaning of section 147 of Act.

The declaration may be filed with respect to foreign assets or foreign income and following amount payable by the taxpayer (declarant) under FAST-DS 2026:

| Sr. No. | Type of assets or income | Conditions | Amount payable |

|---|---|---|---|

| 1 | Undisclosed asset located outside India

Or Undisclosed foreign income |

The aggregate value of the undisclosed asset located outside India and the undisclosed foreign income does not exceed Rs.1 crore | a. 30% tax of the undisclosed value of the asset located outside India as on March 31, 2026.

b. 30% tax on the undisclosed foreign income c. 100% of tax determined in above mentioned (a) and (b) |

| 2 | Foreign Asset acquired from income accruing / arising outside India by declarant when they were non-resident, but such foreign assets were not disclosed in disclosure of foreign assets in their Income-tax return on becoming resident

Or Foreign Asset acquired from income offered to tax in India, but disclosure of foreign assets in Income-tax Return were not disclosed by them |

The value of the asset located outside India does not exceed Rs. 5 crores | Fee of Rs.1,00,000/- |

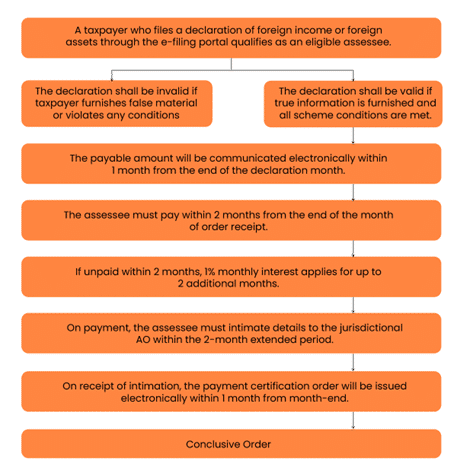

The following infographic outlines the steps for taxpayers to opt in respect of undisclosed foreign assets or foreign income in their return of income

Advantages of Opting Small Taxpayers Scheme (FAST-DS 2026)

The income or amount of investment in the foreign asset which has been declared under FAST-DS 2026 / Small Taxpayers Scheme shall not be included in the total income of the taxpayer (declarant) for any Assessment year (AY) in Income-tax Return under Act or Black Money Act. This is provided that the declarant makes the payment of tax and fee determined under this FAST-DS 2026 / Small Taxpayers Scheme within an extended period of two months along with simple interest at the rate of 1% for every month.

The taxpayer paid tax on foreign income or disclosed foreign assets disclosure scheme under FAST-DS 2026. There will be no rectification or revision of any assessment made under the Act or Black Money Act. Declarant shall not be entitled to claim any set off / relief in any appeal, reference or other proceeding in relation to any such assessment.

The taxpayer shall not be entitled to any refund under tax paid under FAST-DS 2026. Upon making a declaration under FAST-DS 2026 and paying the applicable tax or fee, the taxpayer shall be granted immunity from any further levy of tax, penalty, or prosecution under the Black Money Act in respect of the income or assets so declared for FY 2025-26 or any preceding year.

The Assessing Officer shall consider the declaration made by taxpayer by opting under FAST-DS 2026 while finalizing the assessments which are pending or ongoing assessment proceedings under Act or Black Money Act.

FAST-DS 2026 shall not apply to the following categories:

- Any person directly or indirectly linked to proceeds of crime in respect of whom proceedings have been initiated or are pending under the Prevention of Money Laundering Act, 2002.

- Any person in relation to any income or asset relating to an AY for which assessment proceedings have been completed under the Black Money Act.

Conclusion

FAST-DS 2026 is a compliance window open for resident individuals to regularize the disclosure of undisclosed foreign assets or income. It enables taxpayers to make payment of the applicable tax and, in doing so, obtain immunity from prosecution and penalty under the Black Money Act.

Why Choose Ascentium?

We shall assist assessee / taxpayer who have missed reporting of foreign assets or foreign income or taxed foreign income in their ITR and regularize the undisclosed foreign assets or undisclosed foreign income by making tax payment and filing mandatory forms. We provide clear guidance and the way forward to ensure smooth filing of forms under FAST-DS 2026 and get immunity from prosecution and penalty under Black Money Act. If you have any questions or require assistance regarding our process, please write to us at info@incorpadvisory.in or reach out to us at (+91) 77380 66622.