The International Financial Services Centre (IFSC) of GIFT City represents an opportunity to India to line itself with other international IP hubs like Ireland and Singapore. With an exceptional infrastructure and a highly competitive tax regime, GIFT IFSC has provided a strong platform to own and monetize intellectual property.

Its substantial tax holiday, which is between 20 to 25 years, and a 15 post-holiday tax rate is widely comparable to the actual tax regimes in existing IP jurisdictions (615%), making it more competitive globally. Meanwhile, global IP activity is increasing rapidly. Global patent applications were about 3.7 million in 2024, with a robust 16.5 % growth in India.

Related Read: Global Fund Administration Business: An Overview

Corporates are also moving IP to jurisdictions that have favorable taxes and countries like China have registered almost 1.8 million filings in a single year. With IFSCA’s regulatory framework and recent policy provisions as part of the Budget 2026, GIFT IFSC has already received meaningful involvement of international financial institutions and fintech players demonstrating its increasing relevance as a global hub.

This note discusses the changing international IP environment and studies international tax regimes (including patent box systems and BEPS/Pillar two considerations), comparative jurisdiction, and outlines the business case to understand GIFT IFSC should be a preferred location in terms of IP holding structures

Understanding IPR and IP Holding Structures

IPR Categories

| Patents | Protect inventions |

|---|---|

| Trademarks | Protect brands |

| Copyrights | Protect creative works |

| Industrial Designs | Protect product aesthetics |

| Geographical Indications | Protect origin-linked products |

According to WIPO, IP refers to creations of the mind and underpins innovation-driven economies.

IP Holding Companies

An IP-holding company is an independent legal person that holds licences IP rights on behalf of a corporate group. It is not usually actively involved in production or sales but is apatent/trademark holder or receives royalty or license fees in the affiliates. For instance, a multinational may set up a subsidiary in Ireland to hold and manage its European patents, which are then licensed to its operating entities.

According to one expert, an IP Holding Company or royalty company is established with the express purpose of using, managing and commercializing intellectual property. This architecture allows IP to be centrally managed and may provide tax efficiency. The holding companies are defined as those that own controlling shares of the subsidiaries and are not involved in actual business.

Global IP Trends

The creation and transfer of IP around the world are accelerating. In 2024, the world registered patent applications amounted to approximately 3.7 million, which is an increase of 4.9%. Asia drives this growth: China filed ~1.8M (up 5.5%) and India added 12,274 filings in 2024, a 16.5% jump. The domestic filings of India have now increased in the past eight years. The number of trademark filings (15.2M in 2023) and design filings (1.3M) were also recorded high.

Similar to filings, cross-border IP flows are substantial. As an example, Indian firms paid approximately ~8.8 billion in royalties/technical fees to overseas companies in FY2023. Large Indian companies (Maruti, Nestle, ABB, etc.) declare hundreds of crores of yearly outward royalty payment. On the other hand, foreign companies pay lesser royalties to India. RBI balance-of-payments and OECD statistics indicate that there is an upward trend in technology to import payments.

In the meantime, IP-intensive sectors (biotech, ICT, TMT) continue to see a high influx of FDIs: EDB Singapore lists more than ~S$20 billions of IP/IPR-related projects each year including licensing hubs. WIPO estimates the global licensing worth to be approximately $6.5 trillion in 2023, which is huge value in IP assets.

Patent-box Regimes and Tax Incentives

Countries have responded to these flows by creating patent boxes. Key regimes are summarized in the table. For example, Ireland taxes qualifying patent income in the rate of 6.25%, Singapore in the range of 5-15% under its IP incentive, Netherlands in the rate of 9% at its Innovation Box.

These regimes tend to need large amounts of R&D on the local level (OECD nexus rules) and need extensive networks of treaties. The present incentive offered by India (Sec 115BBF) offers a flat 10% on the domestic patent incomes, but no special rate on foreign IP. Conversely, GIFT IFSC units can take advantage of India DTAs to reduce withholding taxes (e.g. India-UAE 0% patent royalty rate).

| Jurisdiction | CIT (statutory) | Effective IP Tax (patent-box) | Substance Requirement |

|---|---|---|---|

| Ireland | 12.5% | 6.25% on qualifying IP | Must own IP/do R&D locally |

| Singapore | 17% | 5–15% concessional on IP | IP developed /managed in SG |

| Netherlands | ~26% | 9% innovation box | IP owned by NL co + R&D |

| Switzerland | 11–21% | 90% deduction (8.5–12% eff.) | Local R&D and employees |

| Luxembourg | ~24% | 80% IP income exempt (~4.8%) | R&D nexus, IP owned locally |

| Mauritius | 15% | 8-year 100% holiday for patents | IP creation in MU |

| UAE | 0% federal (free zones) | 0% on qualifying IP | IP developed/managed in UAE |

| India (onshore) | 22–30% | 10% on domestic patents | IP domestically created |

| GIFT IFSC (Proposed) | 15% (post-holiday) | 0% during holiday (20 yrs), then 15% | Local functions preferred |

Notable examples: Tech giants like Apple use Ireland as their box; patent licensing (e.g. Phillips) has been a hub in the Netherlands; Singapore is the location of Asia IP HQs (e.g. Nestle, Siemens); Luxembourg was once used to route Amazon EU royalties (EU then tightened rules). These instances reveal how companies are taking advantage of tax and treaty benefits. GIFT IFSC, which offers the same benefits, has the potential to win similar use cases by both Indian and international companies.

BEPS and Substance: International reforms bring about substance requirements to IP regimes. Certainly, OECD/G20 BEPS Action 5/6 and ATAD2 require that patent boxes are only beneficial to income attributed to actual R&D. OECD Pillar 2 (15% minimum tax) implies that countries cannot permanently shield IP income (under 15%). In this manner, the IP regime of GIFT is supposed to fulfill these requirements (e.g. safe harbor with subject-to-tax clauses). On the upside, BEPS compliances render an IP hub credible. GIFT must thus make sure that any tax advantages must show evidence of local IP activity.

GIFT IFSC Background and Development

GIFT is the first planned IFSC in India established by the GIFT SEZ Act (2015) and IFSC Act (2019). It seeks to become a financial, and fintech city like Singapore or Dubai. There are two stock exchanges here: India INX and the GIFT City International Exchange run by SGX with massive volumes every day. In July 2023, the Nifty futures of the Singapore Exchange were transferred to GIFT IFSC.

Tech centers have been established by tech companies like Google in GIFT IFSC. In 2025, the number of financial entities registered is approximately ~1,100. This expansion implies that GIFT IFSC is on a path towards the development of established hubs, and it is time to undertake an IP-holding approach.

Legal/Regulatory Framework in GIFT IFSC

Income Tax: Section 80LA (which has since been changed to Section 147) of the Income Tax Act provides that GIFT IFSC units now have 100% tax exemption in 20 years out of 25 years. The tax rate on income after exemption is 15% while other countries have normal CIT rates of 20-26. GIFT IFSC also provides 10% withholding tax on dividends to foreign shareholders (as compared to 20% cent standard), and no MAT. Such provisions which were strengthened in Budget 2026 ensure that GIFT taxes are comparable to that of Singapore/IP hubs.

IFSC-Specific Laws: GIFT IFSC is governed by the International Financial Services Centers Authority (IFSCA). Companies within IFSC are considered as Indian tax-resident but foreign under FEMA, which allows free cross-border flows.

There are no special IP law and IP holding co regime, but there are normal statutes on IPR in India. Recent IFSCA advice promotes the adoption of IFSC as headquarters: in their 2023 report, they expressly recommend India to establish an IP holding-company regime at GIFT.

Other Regulations: GIFT IFSC units are not subject to customs duties as imports into IFSC are duty-free, and there is no GST on transactions within IFSC.

Stamp duty is waived for transfers to IFSC entities.

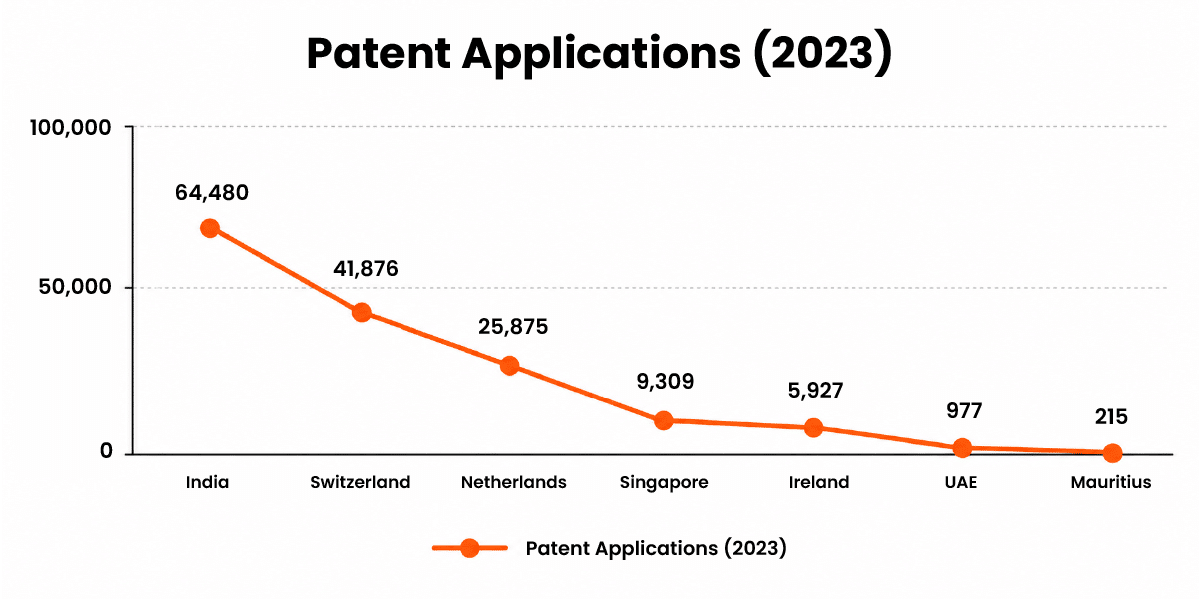

Quantitative Data and Visuals

Key metrics for IP migration are shown below. For example, patent filings by origin (2023) highlight India’s volume:

(Source: WIPO IP Facts 2024)

Why Should GIFT IFSC Host IP-Holding Companies?

Strategic Positioning: The IP holdings hosted by GIFT IFSC would fit the Indian objectives in terms of innovation. It enables R&D-intensive companies (tech, pharma, biotech) to consolidate their intellectual properties using one roof and without taxation. The regime of GIFT IFSC (0% tax in case of a holiday, 15% otherwise) competes with Luxembourg (4.8%) or Ireland (6.25%). This may invert the so-called IP flight of startups that are incorporated overseas. GIFT has been very clearly suggested and encouraged by IFSCA in case of HQs and holding companies.

Tax and Treaty Benefits: GIFT IFSC companies will be able to take advantage of the treaties of India since they are the Indian residents. India-UAE treaty, as an example, exempts patent royalty taxation, which will benefit GIFT-registered IP licensed worldwide. Moreover, the extended holiday of GIFT IFSC eliminates corporate tax burden of India for over 20 years. Practically, royalties that are transferred via GIFT firms may be tax-free, 0% in IFSC, with credit provisions under Pillar Two. This is comparable to those of the Netherlands (0% dividend WHT) or Ireland (6.25% on IP).

Substance and Governance: GIFT IP-holding companies must have real substance to comply with BEPS: e.g. local R&D workers, GIFT management. This can be fulfilled by the good workforce of STEM in India and the professionals of IFSC existing there. IP boards may be required to be co-located by GIFT, which is compatible with OECD nexus tests. IFSCA may also support the necessary IP activity: e.g., by hosting common R&D laboratories or offering co-working space to manage patents. GIFT-based IP structures will be credible to the international tax authorities due to good governance (annual audits, accounting transparency).

Operational Efficiency: The current financial ecosystem in place by GIFT IFSC including banks exchanges, fintech platforms offer ancillary services to IP firms or IP holding companies (funding, licensing, financial transactions). An example of this would be an IP fund that is owned by IFSC and licence patents and shares the profits using tax neutral funds offered by GIFT. The operational support including easy company incorporation, fintech sandbox is already established, and, thus, an IP-holding company can be established without burdensome approvals.

Conclusion

GIFT IFSC has the potential to emerge as India’s preferred jurisdiction for intellectual property holding and monetization, aligning itself with established global IP hubs like Ireland, Singapore, and Luxembourg etc. With a long-term tax holiday, competitive post-holiday tax regime, treaty access, and a robust regulatory ecosystem, it offers a compelling platform for global and Indian businesses to centralize and commercialize IP assets. As global tax rules increasingly demand substance and governance, GIFT IFSC provides an opportunity to build credible, compliant, and efficient IP holding structures. For innovation-led businesses, it can become a strategic base for protecting, licensing, and scaling intellectual property globally.

Why Choose Ascentium?

At Ascentium, we help businesses build structure, establish, and operationalize IP holding platforms in GIFT IFSC with a practical and commercially focused approach. Our team combines expertise across IFSC regulations, international tax, FEMA, transfer pricing, IP ownership structuring, and cross-border licensing models etc. From evaluating the right jurisdictional fit to entity setup, tax optimization, regulatory approvals, and ongoing compliance, we provide end-to-end support. We focus on creating sustainable IP structures that are not only tax efficient but also aligned with global BEPS, Pillar Two, and substance requirements. To learn more about our fund services, you can write to us at info@incorpadvisory.in or reach out to us at (+91) 77380 66622.

Sources

- https://business.gov.nl/finance-and-taxes/deductibles-and-schemes/how-to-use-the-innovation-box/

- https://ifsca.gov.in/Document/10_EY-GIFT_tax_benefits_050225.pdf

Authored by:

Naresh Tunvar | GIFT City