Over the years it has been observed that companies forming a part of large group holding structure, undertaking investment activity as core business activity, increasingly face risk of being classified as Non-Banking Financial Company (NBFC) owing to the nature and composition of their assets and income streams. NBFC is a financial institution (company) registered under Companies Act 2013 that carries on the business of financial activity— such as collection of deposits from public, advance loan, finance customer, MSMEs, as its ‘principal business’ and requires to be registered with Reserve Bank of India (RBI) under Section 45IA of the RBI Act, 1934.

To determine whether financial activity constitutes the ‘principal business’ of an entity, the RBI has prescribed the well-established ‘Principal Business Test’ (commonly referred to as the 50-50 test). Pursuant to this test, a company is regarded as an NBFC if it satisfies both of the following conditions, irrespective of nature of activities undertaken:

- Financial assets exceed 50% of total assets and

- Income from such financial assets exceeds 50% of total income

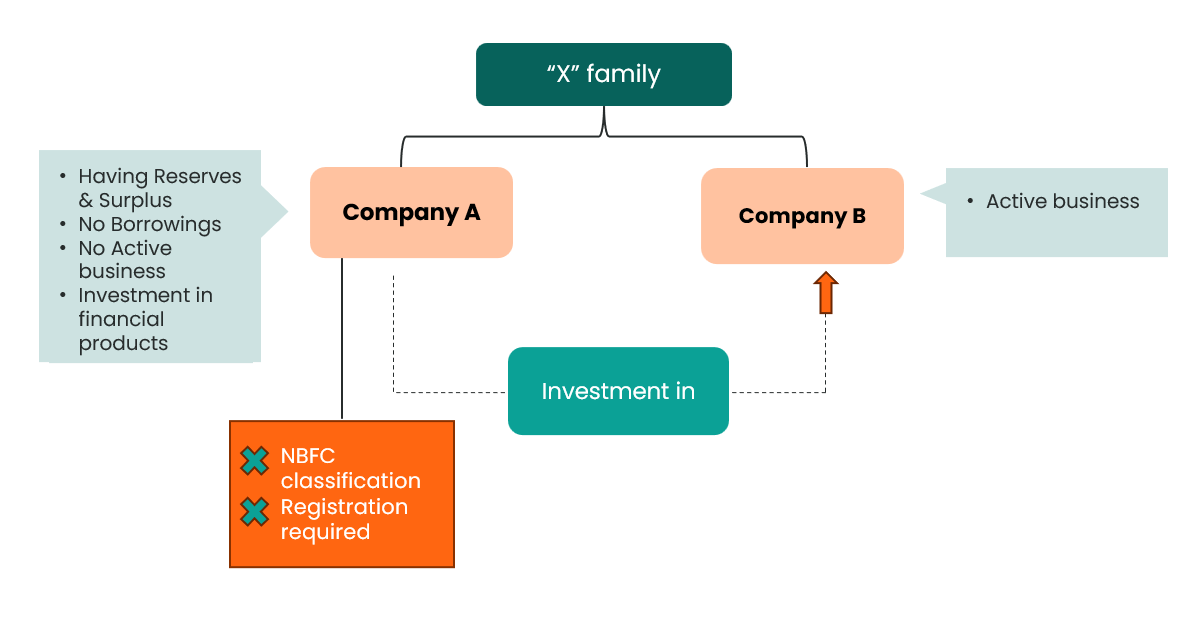

Companies in a promoter group that mainly hold investments in group companies or financial products can get classified as NBFCs if they meet the ‘principal business’ test, even if they do not lend or accept deposits.

Related Read: Are Nominations Enough for Succession: Explained

Since NBFC status brings significant regulatory compliance, such companies often create ancillary operational activities to generate non-financial income thereby overshadowing the true substance of their financial activities. It has been observed that certain group structures use layered partnership firms or LLPs beneath holding companies for investment and asset-holding purposes.

Such arrangements are often intended to achieve tax efficiency, including mitigation of dividend tax implications, while retaining strategic investment control within the promoter or family group. Such arrangements may also facilitate segregation of investment activities from core operating businesses and enable flexible deployment of capital for future investments and expansion initiatives.

Regulatory Shift by RBI

To address this issue, The Reserve Bank of India (RBI) through its amendment in RBI (Non-Banking Financial Companies – Registration, Exemptions and Framework for Scale Based Regulation) Amendment Directions, 2026, has just introduced significant changes to its NBFC regulations, effective from July 1, 2026. While changes are technical in nature, these updates have major implications for family offices/groups structures to manage investments, particularly through holding companies.

Introduction of ‘Unregistered type I NBFC’:

RBI has introduced a New Category for very small & Low-Risk NBFCs. The key differentiators for this new category are:

- They do not accept public deposits.

- They do not deal directly with external customers.

- Their asset size is below INR 1,000 crore.

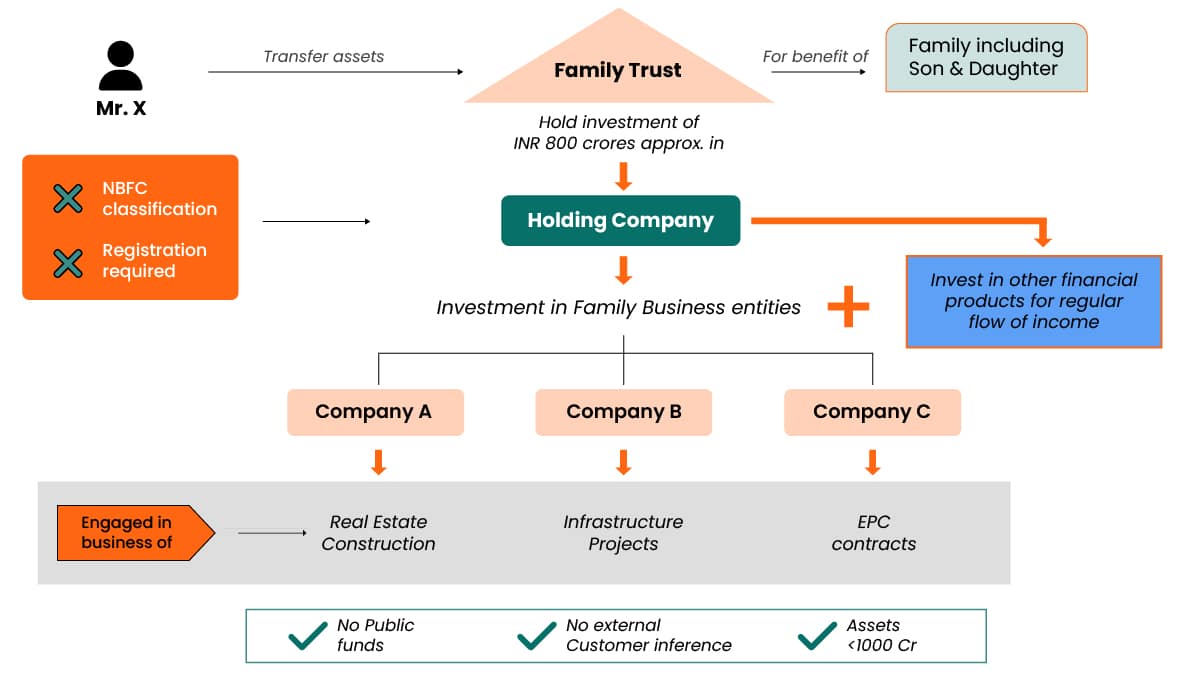

Entities fulfilling all the above prescribed conditions will now be termed ‘Unregistered Type I NBFCs’ and, crucially, can be exempted from registration and maintaining reserve fund requirement under Section 45IA and 45IC of the RBI Act, 1934 respectively, from July 1, 2026. This is a game-changer regulation for many family-owned investment vehicles in holding company structure that fit this description.

Related Read: Why Women Should Make a Will: A Complete Guide

The most important consideration of the amendment for the investment company is that if such company intends to invest in overseas in a financial service section, will likely still require RBI registration as type I NBFC and approval.

Under the broader framework laid down by RBI, Type I NBFC is one that satisfies the same no-public-funds and no-customer-interface profile but holds a Certificate of Registration from RBI.

Why This Matters for Family Investment Structures?

Earlier, small size/mid-size family offices in corporate structure such entities engaged in financial activities – holding shares, debenture or any other financial instruments etc. – were required a registration with RBI under NBFC regulations bringing with it significant compliance burdens, despite their though Assets Under Management (AUM) being less than INR 1000 crores approx. Consequently, these regulatory requirements often acted as a constraint in efficiently structuring investment operations.

Even within group companies, establishing a separate entity to hold investment belonging to the promoter group was often not feasible considering the rick of being classified as NBFC. As a result, investments were typically parked across different structures.

The new framework changes this – these family investment structures now have a clear path to potentially simplify their regulatory overhead. A family holding company which in turn holds various investments across different group businesses or external portfolios, would qualify for exemption if following criteria are fulfilled:

- Funded entirely by family members/family trust from self-generated sources (including group entity / Company with sufficient Reserves and Surplus and no borrowing etc.),

- Serves no external customer and

- Maintain asset size below INR 1000 crores,

However, if multiple companies exist within the group structure, then their assets are added together for asset test. This measure is intended to curb the regulatory arbitrage by preventing large promoter groups from fragmenting their investments across entities to remain below threshold.

One limitation that family offices will face is that investment in overseas financial services entities may trigger mandatory registration requirements, thereby limiting global investment opportunities.

Overall, this amendment offers most significant benefits for family-owned investment companies, reduction in administrative and compliance costs, and general regulatory complexities. By giving the opportunity of deregistration to the eligible entities, RBI alleviates the burden of extensive compliances, thereby allowing family offices to focus more on wealth preservation and growth.

Navigating the New Landscape: What You Need to Do?

While this offers relief, it’s not a free pass. To benefit from this relaxed regime, entities must:

- Annual Board Resolution: Pass a board resolution each year affirming that it will not accept public funds or have external customer interaction.

- Disclosure in Financial Statements: Clearly disclose its ‘Unregistered Type I NBFC’ status in its financial statements.

- Auditor Reporting: Ensure its statutory auditor reports any violations of these conditions.

- Asset Test: Strictly adhere to the INR 1,000 crore asset limit. If there are multiple qualifying NBFCs within the same group, their assets will be clubbed for this test.

Clean Exit from RBI Oversight?

This is a relaxation and not a complete removal. RBI has just stepped back from registration and not from overall oversight. The relief has received only with respect to registration and maintenance of reserve fund and not from other relevant provisions of Chapter IIIB of the RBI Act, as well as other applicable laws. However, the RBI still retains the authority to issue directions and take action against these entities when necessary.

Possible structures1 that one can think of post July 1, 2026:

Structure A- Family-owned funding framework through investment

Key Considerations

- Greater flexibility in managing investments and capital deployment.

- Reduction in dependence on external borrowings

- Better treasury management and focused business operations.

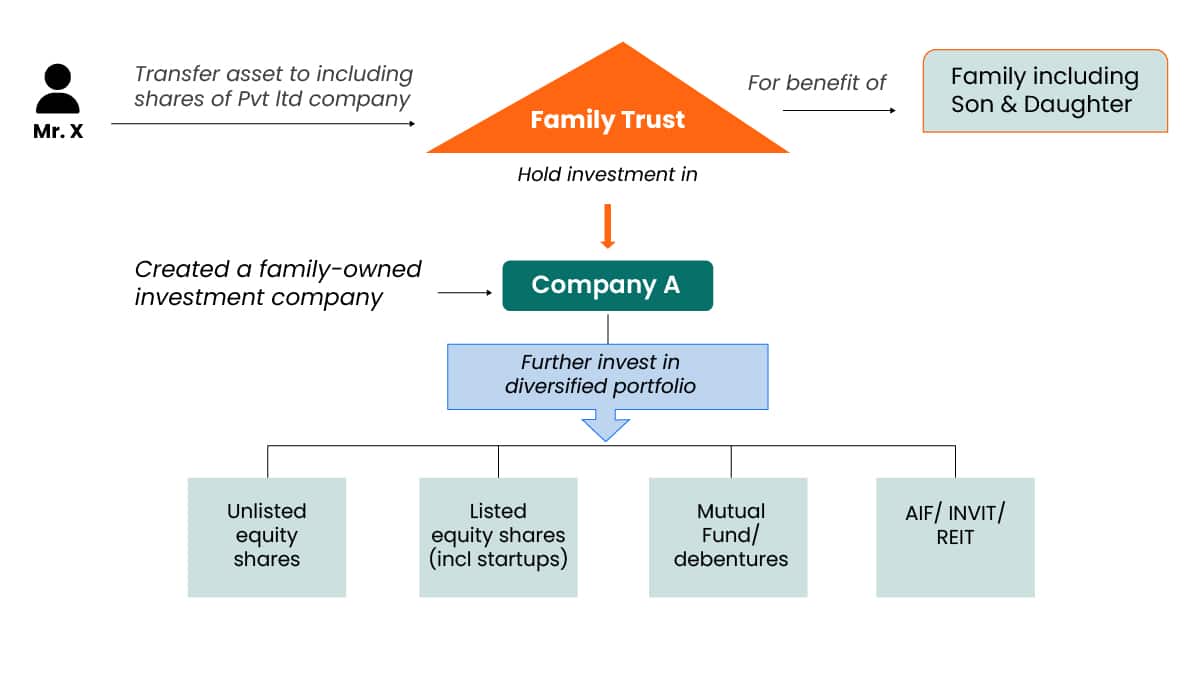

Structure B- Family Trust–Holding Company Structure for Succession Planning and Strategic Investments

Key Considerations

• Family offices can focus more on wealth preservation and growth

• Separation of family investment and business will be useful for strategic expansion through mergers & acquisition and IPO.

Structure C

Key Considerations

• Centralised family investment vehicle for managing and deploying family wealth through a dedicated investment company.

• Family investments under one entity for monitoring, reporting and decision-making.

• Help in focused wealth preservation, investment management and risk allocation.

All the above possible scenarios are subject to RBI regulations and other applicable regulations including FAQs.

Conclusion

For family offices, this amendment presents a regulatory tailwind worth capturing. The proposed framework offers regulatory relief for genuinely low-risk captive entities. Groups with pure treasury or investment holding companies operating solely on owned funds, and not engaged in lending, guarantees, or financial product distribution, may benefit from reduced compliance associated with maintaining an RBI certificate of registration.

This regulatory shift is a timely opportunity to establish a dedicated holding company as their primary investment vehicle, the landscape has never been more accommodating for privately funded, internally managed structures. It is equally a moment to revisit existing group arrangements and streamline them, whether by consolidating entities or restructuring altogether, to leverage these new provisions for greater efficiency and compliance.

Effective date: July 1, 2026. Consult your legal and compliance advisors before restructuring.

Why Choose Ascentium?

At Ascentium, we understand that structuring of family office can be complex and challenging. Our dedicated family office management experts offer comprehensive, tailored solutions and is committed to safeguarding wealth, optimizing tax outcomes, and enabling smooth intergenerational transitions. To learn more about how we can support your family office needs, write to us at in-info@ascentium.com or reach out to us via WhatsApp at (+91) 77380 66622.

References

1 Above structures must be evaluated on case basis considering Companies Act 2013, Income Tax Act 2025 and other applicable laws.